Shares of Deutsche Bank (NYSE:DB) have come under increasing pressure this year after a spate of high-profile bank failures on both sides of the Atlantic. After the fire sale of Credit Suisse (CS), the market is indicating fears that DB might be next. There are several issues at stake, continuing a pattern where bank executives’ and regulators’ gambits to show strength have backfired. The proximate cause of the latest fears seems to be Deutsche Bank’s decision to redeem some junior bonds in an attempt to show strength. But before that, an unusual decision by Swiss regulators to pay equity holders of Credit Suisse while stiffing junior bondholders seems to be causing some serious unease in Europe. This fueled the belief by traders that politics would trump property rights, and led to big selloffs in bank debt across the EU. EU regulators were reportedly upset about the Swiss favoring shareholders over bondholders, and it showed in their statements to try to ease investor fears. The worry over Deutsche could be much ado about nothing, but it’s worth diving into why they’re under pressure.

Deutsche Bank: What We Know

- In a problem common to many banks that operate in Europe, Deutsche Bank has had a poor return on assets and equity for quite a while. This has been a problem with European banks for a long time, and crazy policy experiments like negative interest rates made this worse. DB isn’t as bad as Credit Suisse, which had a negative return on equity, but European banks generally aren’t cash cows. I’m showing a return on equity for DB of about 7%. DB trades for about 0.25x book value right now, implying a high return for shareholders if they can turn things around. Deutsche has been undergoing a turnaround plan that has seen dramatic cost cuts, but the bank still has struggled to raise its return on equity to target levels.

- As with the Fed, inflation has forced the ECB to raise rates. But that’s a problem if it means depositors flee banks holding a bunch of negative interest rate bonds and put their cash in money market funds because the banks won’t have the money to pay depositors. The problem the US has with banks that took too much risk with depositors’ money also is a problem in Europe. For strong banks that managed risk well, this isn’t much of an issue because they can earn more interest income for themselves. But for weak banks that are overleveraged, it’s highly problematic.

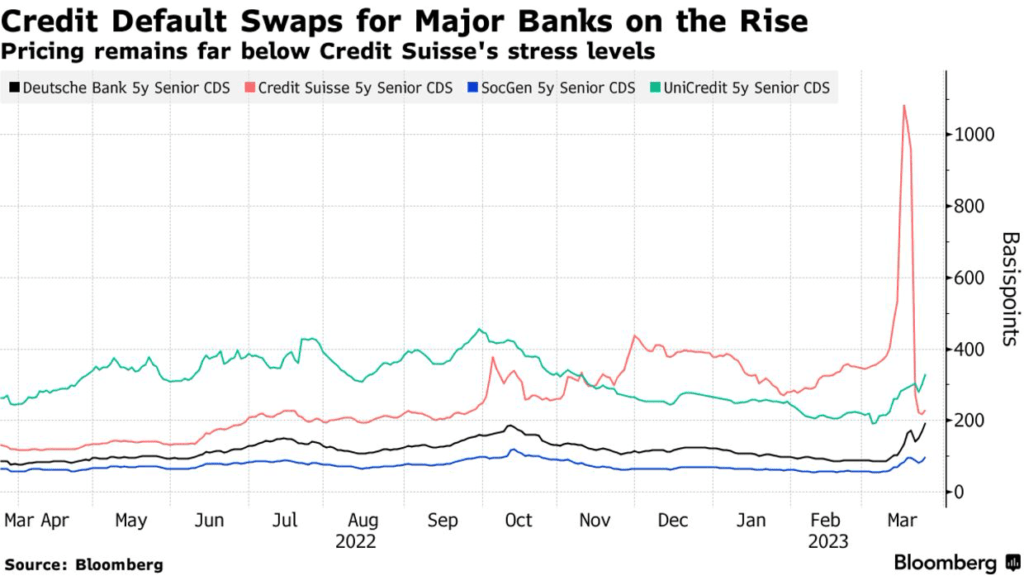

- DB credit default swaps aren’t showing too much stress, but they’re worth watching. Overall, the market is more worried about UniCredit (OTCPK:UNCRY), the second-biggest bank in Italy. This is getting fewer headlines however, because fear over DB is rising while fear over UniCredit has eased a little.

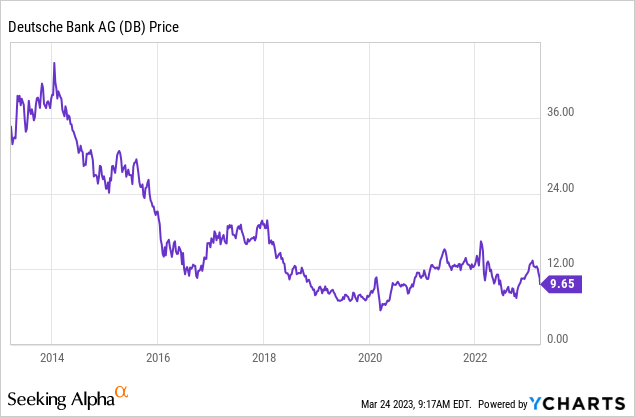

- As of my writing this, Deutsche seems to have bounced off the lows. The stock was previously down about 15%, while now it’s only down about 5%, at least for the ADRs in the US. Overall, Deutsche doesn’t look that bad as a business, but it’s not a great one either.

What We Don’t Know

- Bank runs have a way of becoming self-fulfilling prophecies. Deutsche’s business doesn’t look great, but it’s priced attractively for a turnaround. However, if the market decides that Deutsche is a bad risk and makes it difficult or impossible for the bank to raise capital, then things can spiral downward. It doesn’t necessarily help when politicians come out to say banks are “very profitable,” or “very strong.” Strong words are weakness – no words are strength.

- We don’t know if Deutsche has some monsters in its closet. A few years back, American regulators in particular flagged Deutsche as exceptionally risky – the company took a series of steps to deleverage but it’s not clear whether the company has been able to fully remedy this. Deutsche’s leverage ratio appears to have fallen by about half since then and their credit rating has been upgraded, but it’s still too high for investor comfort at around 25x. These could come from derivatives exposure, loans, or FX, and any misstep the bank makes drives the leverage ratio higher.

- We don’t know how regulators will react in the US and in Europe. The trouble with buying global bank stocks right now is that it only takes one country to decide to stick it to banks and let a big bank fail to bring the entire global system under a ton of pressure. The Swiss did a reasonably good job of containing the Credit Suisse fallout, but there’s no guarantee that every single country that sees banks under pressure will do as good of a job. This is at the core of why the market got so worried about Credit Suisse’s contingent bonds getting wiped out while the equity holders got paid some money.

What This Means For Your Money

Right now, there’s not too much cause for concern that Deutsche Bank will suddenly fail and cause a financial crisis in the US or Europe. But there are a few takeaways that investors should keep in mind. First, stress in the banking system calls into question why investors are paying such a high multiple for stocks at 18x on the S&P 500 (SPY). Second, volatility has risen rapidly in the markets at the same time central banks have hiked rates, making holding cash more attractive for the short term vs. stocks. Third, the market is offering up some potential opportunities, with money flowing into stocks like Apple (AAPL) regardless of price and fleeing stocks like banks. Common and preferred shares of too-big-to-fail banks could be worth a look for investors with a strong stomach. As for Deutsche Bank, I wouldn’t buy or sell it, but I’d watch the situation to see if it’s indicating more serious problems in the financial system than we’ve come to understand thus far.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Article by Logan Kane, https://seekingalpha.com